Bank Account Bonus Timing

Anytime we write about bank bonuses, one of the first questions we hear is, “When can I close this [new] account?” That's a super important question to always ask yourself, but perhaps not for the reason you think. You see, I recently learned a very hard lesson about bank account bonus timing. It involved one of my all-time favorite bank account bonuses, which I have done many times and one we regularly write about: the U.S. Bank $1,200 business checking offer. Whatever you do, don't be me. Do not lose $1,200 over a simple mistake. Here's what happened.

The Bank Bonus

Back in January, I decided it was time to open another U.S. Bank business checking account for that sweet $1,200 bonus. The requirements for the bonus are minimal:

- Deposit $25,000 within 30 days of account opening;

- Leave $25,000+ deposited for 60 days; and

- Complete 6 qualifying transactions within 30 days of account opening.

Overall, it is pretty simple. No one can really screw this one up. Right? RIGHT? Nope, I totally forgot about bank account bonus timing and ran into some issues.

The Process

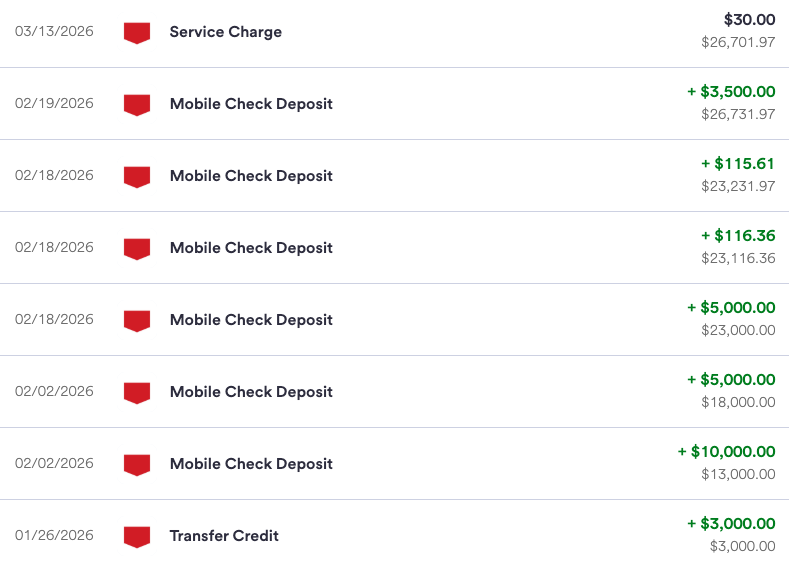

As soon as the account was opened, I deposited $3,000. Over the next 20 days or so, I completed 6 mobile check deposits, which were explicitly listed as qualifying transactions. By day 24 from account opening, I had $26,700+ deposited, had completed my 6 qualifying transactions. I should have been good to go. I then waited until 60 days from account opening (3/27/26) for all the requirements to be met. Since I was charged a fee on 3/13/26 (for not holding an average daily balance in February of $25,000+), I expected the bonus to post on my 4/13/26 statement.

The only problem is that no bonus posted on the 4/13/26 statement. Then no bonus posted on the 5/13/26 statement. I knew something was up, but I wasn't sure what I had missed. Maybe my timing was off? Perhaps I incorrectly believed mobile check deposits worked? In any event, I had to wait until we were home from our big Scotland trip to inquire. Once I did that, I realized my dumb mistake.

My Mistake: Bank Account Bonus Timing

U.S. Bank History

Previously, we'd used a U.S. Bank Business Checking account for ToP activities. We received a nice big bonus for opening that account, but that was back in 2023 or 2024. Since that time, that LLC had no banking activity with U.S. Bank. The other accounts we've opened there were in other business names and with Sarah as the underlying person. So what was the issue? I had to get to the bottom of it, so I called U.S. Bank to find out.

Investigation

The very helpful telephone representative confirmed a coupon code for the $1,200 bonus was attached to the account. She then confirmed $25,000+ was deposited within 30 days of account opening and remained deposited through the 60th day of account opening (and beyond). The agent then confirmed that mobile check deposits are considered qualifying transactions and that I had I met the minimum transaction requirement. Like me, she was confused. She said she needed more time to investigate. Unfortunately, her investigation revealed my big blunder: U.S. Bank does not care about the timing of receiving bank bonuses, rather about timing of opening and closing accounts. The specific language in the terms & conditions of this offer is: “[e]xisting businesses with a business checking account or had one closed within the past 12 months, do not qualify.“

Lesson Learned

D'oh! There it is. It did not matter that the business last received a U.S. Bank bonus in 2024. Rather, the problem was this business didn't close its prior account until February 18, 2025. I was 23 days shy of 12 months from closing the prior account when I opened this account. Yep, 23 days cost me $1,200. Actually, my terrible lack of digging through the T&C and verifying the closure date of the prior account cost me $1,200. This mistake is really, really simple to fix and, honestly, inexcusable. I certainly will never let this happen again!

Bank Account Bonus Timing: ToP Thoughts

So, what is the answer to the often-asked question, “When should I close this [new] checking/savings account?” The answer is: As soon as possible after receiving the bonus. For accounts like the U.S. Bank Business checking accounts, the faster you close it means the faster you can reopen it. For other accounts, base eligibility upon receipt of the bonus means the clock is already ticking before closure. Overall, I learned a big lesson with this bank account bonus timing snafu. It is not a mistake I will make again any time soon. I am now tracking all bank account opening and closing dates, to make things simple for my future self.

How about you: Have you ever messed up a bank account bonus? Come over to our Facebook group and let us know.